Parimaid praktikaid Euroopa Personalijuhtimise Ühingust (EAPM) (inglise keeles)

PARE kuulub Euroopa Personalijuhtimise Ühingusse (EAPM) ja selle sarjaga toome PARE liikmeteni parimaid praktikaid iganädalasest EAPM-i uudiskirjast, mille koostamisele aitavad kaasa EAPM-i töörühmad. Septembrikuu uudiskirjas räägiti lähemalt Euroopa Liidu sotsiaalõiguspoliitikast ja sotsiaalsest aruandlusest.

NB! Artiklid on inglise keeles ja need on koostanud EAPM-i Euroopa Liidu töörühm.

Pildil on EAPM-i juhatuse liikmed.

Reflections on European social legislation policy 2019-2024

Social policy has a long history in Europe. During the 1972 Paris Summit, the governments of the then European Community’s Member States charged the Commission with developing a proposal for a first Community Social Action Plan. Susannah Haan reflects on European social legidlation policy from recent years:

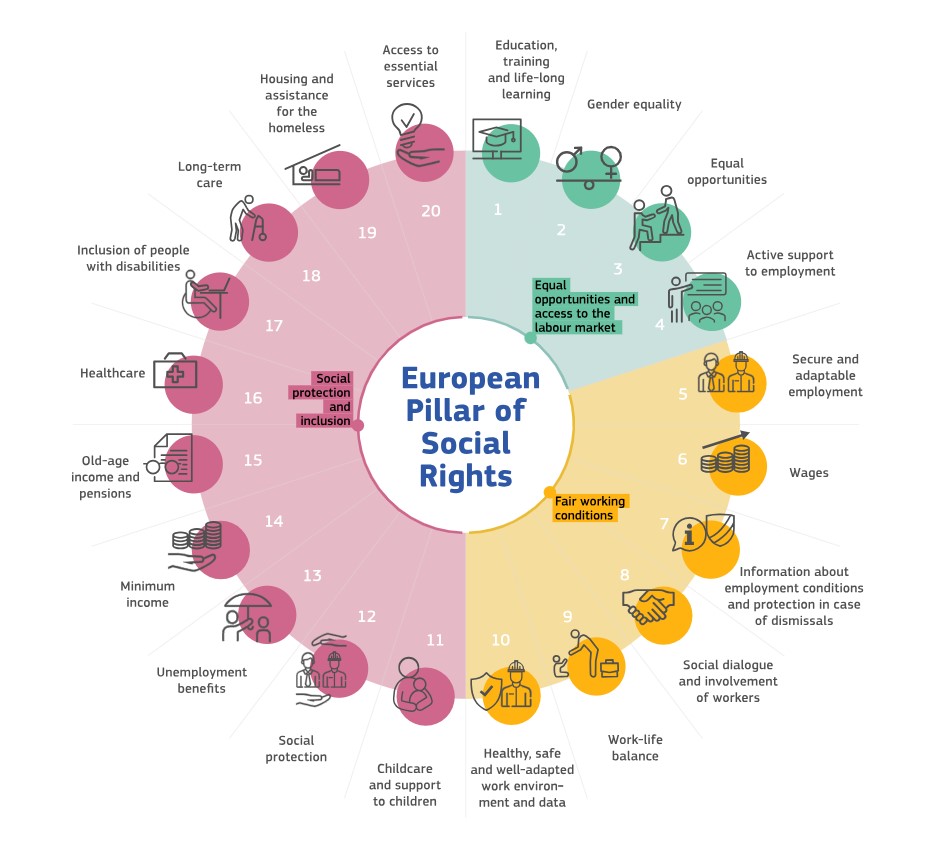

More recently, the 2017 European Pillar of Social Rights Action Plan covered 20 issues across 3 key areas:

- Equal opportunities & access to labour market (education, training, lifelong learning, gender equality, equal opportunities, active support to employment)

- Fair working conditions (secure & adaptable employment, wages, information about employment conditions and protection in case of dismissals, social dialogue and involvement of workers, work /life balance, health & safety)

- Social protection & inclusion (childcare, social protection, unemployment benefits, minimum income, pensions, healthcare, disabilities, long-term care, housing, access to essential services).

Actions taken by the European Commission 2019-2024 led by Ursula von der Leyen include the following social policies.

Equal Opportunities & Access to labour markets

The European Commission established a separate Commissioner for Equalities, and developed EDI strategies in the following areas in 2020:

- Gender Equality Strategy

- Anti-Racism Action Plan

- Roma Strategic Framework

- LGBTIQ Equality Strategy

- Disability Rights Strategy.

Legislation has been developed including:

- 2022 Women on Boards directive

- 2023 Pay Transparency directive

- 2024 Gender-based violence against women directive

On education & training, the EU declared a Year of Skills and developed its Skills Agenda, which aimed to:

- strengthen sustainable competitiveness, as set out in the European Green Deal

- ensure social fairness, putting into practice the first principle of the European Pillar of Social Rights: access to education, training and lifelong learning for everybody, everywhere in the EU

- build resilience to react to crises, based on the lessons learnt during the COVID-19 pandemic.

Fair working conditions

Policy on fair working conditions includes health & safety at work, work/life balance and social dialogue.

The Communication on Safety & Health at Work Strategic Framework 2021-2027 focuses on three cross-cutting objectives:

- anticipating and managing change in the new world of work brought about by the green, digital and demographic transitions;

- improving prevention of workplace accidents and illnesses;

- increasing preparedness for any potential future health crises.

This includes greater focus on mental health and healthy workplaces.

The 2019 Work-life balance for parents and carers directive set out the right to paternity, parental and carers’ leave and to flexible working arrangements.

The 2023 Initiative on Social Dialogue stresses the importance of freedom of association and collective bargaining as fundamental rights in EU law.

Social protection and inclusion

Work on social protection and inclusion includes the following:

- 2022 Recommendation on Long-Term Care

- 2022 Minimum Wage Directive

- 2023 Recommendation on Minimum Income

In addition, there have been new developments on social reporting.

Future direction of travel

In 2024, the Belgian Presidency has sought to develop further agreement on the future direction of social policy for the next Commission in 2024-2029. In April 2024, a majority of Member States signed a declaration on social policy. However, there was some opposition from some Member States and members of the business community, citing concerns that the EU approach focuses only on regulation and not regulation and competitiveness. Given the large volume of regulation passed under the EU Green Deal, many businesses are struggling to understand and implement all of the new rules.

The future direction of EU social policy will depend on the new Commission and parliament post elections in June 2024.

Social Reporting (non-financial / sustainability reporting)

There have been considerable developments on social reporting legislation as part of the Capital Markets agenda, mandating certain disclosures to investors. Social reporting is considered to be one of the 3 pillars under ESG: Environmental, Social and Governance disclosures, which together form non-financial reporting.

Key social reporting in EU legislation includes:

- 2014 Non-Financial Reporting Directive (NFRD)

- 2022 Corporate Sustainability Reporting Directive (CSRD)

- 2023 European Sustainability Reporting Standards (ESRS), secondary legislation under the CSRD

- 2024 Corporate Sustainability Due Diligence Directive (CS3D), due to be adopted in April 2024

Non-Financial Reporting Directive

The EU Non-Financial Reporting directive (NFRD) applies to large ((i) > 500 employees and (ii) > €20M total assets or > €40M net turnover) public-interest entities (PIEs) i.e. listed companies, financial institutions and insurance companies on a number of ESG aspects (broadly defined, subject to interpretation, including environment, social, human rights, corruption) and other information related to business model, description of policies, results, main ESG risks and KPIs.

After a few years of operation, its limitations were perceived to be:

- No definition re how to report on these ESG aspects: companies are free to use voluntary frameworks and standards (UNGC, SDGs, GRI, SASB, TCFD amongst many others)

- Leaves significant flexibility to Member States to transpose into national law, including on:

- where information should be reported in corporate reporting,

- whether audit of sustainability information is mandatory or not,

- whether some companies should be excluded from scope based on legal form, etc.

This resulted in what was perceived by policymakers to be content that was too diverse, which did not meet investor demands for high quality information that is reliable and comparable. This led to demands for the Corporate Sustainability Reporting Directive.

Corporate Sustainability Reporting Directive

The EU Corporate Sustainability Reporting directive (CSRD) entered into force on 5 January 2023. The aim is to enable investors to understand the material impacts caused by the company, both financial and societal impact.

- The first companies (including non-EU subsidiaries already subject to NFRD i.e. 500+ employees) will have to apply the new rules for the first time in the 2024 financial year, for reports published from 1 January 2025.

- Large companies (including non-EU companies) with 250+ employees will need to report in 2026 on 2025 financial year.

- Quoted companies will need to report in 2029 for 2028 financial year if not already covered above (reporting encouraged from 2026).

- Small credit institutions and insurers will need to report in 2027 for 2026 financial year.

- Non-EU parent companies with a strong EU presence via subsidiaries or branches will need to report in 2029 for financial years starting 2028.

New requirements under the CSRD include:

- Third-party audit / assurance.

- Integrated reporting in one ‘consolidated management report.

- Digital tagging in a machine-readable ‘XHTML’ format.

- Standardised reporting as defined in the European Sustainability Reporting Standards (ESRS).

Double materiality principle: consider impact on business and on stakeholders.

European Sustainability Reporting Standards

The EU published its own sustainable reporting standards in December 2023. These cover different areas of ESG reporting:

– 5 Environmental standards on climate change, pollution, water & marine resources, biodiversity & ecosystems, resource use & circular economy.

– 4 Social standards on own workforce, value chain, affected communities, consumers & end uses.

– Governance standard on business conduct.

Corporate Sustainability Due Diligence Directive

This was the most contentious dossier and was finally agreed in April 2024, requiring:

- companies to undertake due diligence on human rights and the environment,

- mandates stakeholder engagement, grievance mechanisms, remediation measures,

- a climate plan in line with the Paris agreement (limiting to 1.5 degrees)

It also introduces liability and sanctions for breaches that lead to harm.

It will apply to companies with 1000 employees and 450m turnover, both EU and non-EU operating in Europe. Implementation will take place from 2027-2029, depending on the size of the company:

2027 5000 employees / 1500m turnover

2028 3000 employees / 900m turnover

2029 1000 employees / 450m turnover.

The final text should be published in the Official Journal shortly.

Companies will need to:

- Set up co-ordination across teams (board, legal, procurement, etc)

- Identify your sustainability obligations

- Benchmark your current policies & processes

- Identify gaps and build steps to comply

- Draw up updated policies and processes

- Train your people.